The GTA Housing Market Is Coiled — But Not Cleared for Rebound

Spring 2026 is not a collapse story, and it is not a recovery story either. It is a market where supply is pulling back faster than demand is returning — leaving conditions tighter, but still fragile.

February 2026 GTA Snapshot

If you only read the headline version of the February numbers, you could talk yourself into believing the Greater Toronto Area housing market is finally turning. That reading is too generous. The more accurate view is narrower and less comfortable: the market has tightened at the margin, but it has not recovered.

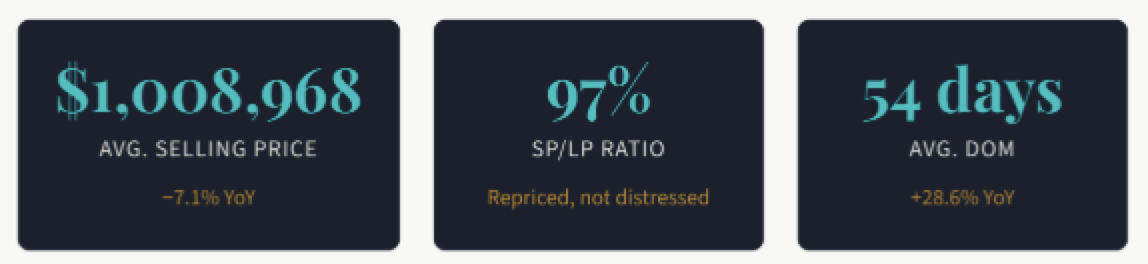

February 2026 GTA home sales came in at 3,868, down 6.3% year over year. New listings fell harder, down to 10,705, a 17.7% annual decline. Active listings still sat at 19,314. The average selling price was $1,008,968, down 7.1%, while the MLS HPI composite benchmark was down 7.9% year over year.

It is a market where sellers are stepping back faster than buyers are stepping in. Less new supply does not automatically mean strength. Sometimes it simply means owners do not like the pricing environment enough to list.

The market is tighter, but still clearly negotiable

Structure matters more than the headline

The cleanest way to read this market is through structure, not press-release language. Across all TRREB areas, the sales-to-new-listings ratio was 33.6%, months of inventory were 5.0, the average sale-to-list price ratio was 97%, average listing days on market were 36, and property days on market were 42.

Those are not seller-market conditions. They describe a market where buyers still have room to negotiate and where pricing discipline matters far more than generic spring optimism. Yes, the market tightened relative to last year because new listings fell faster than sales. But less loose is not the same thing as healthy. A market can tighten mechanically while still being fundamentally soft.

The GTA market has tightened at the margin, but it has not recovered.

That is still well inside buyer-leaning territory. It does not support a broad seller-market narrative.

Inventory is not scarce enough to create widespread urgency. Buyers still have decision time.

The original pressure thesis was not wrong

What still holds

The strongest part of the earlier “coiled market” thesis still holds. This is not a distressed market. Sellers are not capitulating in large enough numbers to create disorder. There is no sign of broad forced liquidation. The more accurate description is a market under pressure, with participants still trying to avoid realizing weakness unless they need to transact.

That is why some neighbourhoods and some product types still feel tighter on the ground than the broader market data might suggest. It also explains why the market feels conflicted. It is soft in the aggregate, but not broken at the street level. Scarce, well-priced homes can still trade properly. The problem is that this does not describe the whole market.

What changed is not the micro read. It is the macro overlay.

Why the timing call needed correcting

The reason the original version needed tightening is simple: the timing call was too aggressive. A rebound in housing is not powered by lower rates alone. It needs confidence, and confidence is still weak.

The Bank of Canada held its policy rate at 2.25% on January 28, 2026. More importantly, the Bank was explicit that the outlook remains vulnerable to unpredictable U.S. trade policies and geopolitical risks, and that the Canadian economy is still adjusting to U.S. tariffs and the new global trade landscape, with growth expected to remain modest.

That is not the language of a clean macro backdrop. So yes, rates are off the highs. But that alone is not enough to unlock a broad demand return when the surrounding economic picture still feels unstable.

The market is coiled in a structural sense, but the release valve has not opened because macro confidence is still missing.

Financing is less painful than at peak tightening, but not loose enough to override broader uncertainty.

Trade friction and Middle East risk matter because they feed uncertainty, inflation risk, and household hesitation.

Labour conditions are not supporting a clean spring bounce

Why unemployment matters in a housing cycle

The labour market is another reason to stay disciplined. Statistics Canada reported that Canada’s unemployment rate rose to 6.7% in February 2026, while Ontario’s unemployment rate rose to 7.6%. On the ground, that matters because housing demand does not disappear when employment weakens, but it does become more selective, more cautious, and more price-sensitive.

That is exactly what the GTA data is showing now. First-time buyers hesitate. Move-up buyers become defensive. Investors become harder to motivate. The result is not a dead market. It is a thinner market.

- Lower confidence weakens urgency.

- Higher uncertainty raises price sensitivity.

- Selective demand rewards A-grade homes and punishes mediocre listings.

Ontario still has too much inventory to justify a bullish provincial read

The GTA does not operate in isolation

The provincial backdrop still looks heavy. OREA and CREA reported that Ontario had 24,145 new residential listings in February 2026, down 11.6% year over year, but still had 49,884 active listings at month-end — the highest February inventory level in more than a decade. Months of inventory were 5.3, well above the long-run average of 2.6 for this time of year.

That matters because even if GTA listing flow has started to contract, the broader Ontario market still carries enough inventory to limit how aggressive you can be with a rebound narrative.

Where the weakness still sits inside the GTA

Detached is holding better. Condos are still the weakest link.

The GTA is not one market. It is several markets moving at different speeds. The February tape is not just a condo problem, although condos remain the weakest major category.

TRREB’s February breakdown shows 1,683 detached sales at an average price of $1,325,654, versus 1,088 condo apartment sales at an average price of $626,650. Detached is holding up better, but that is relative resilience, not strength. Condos remain the most obvious soft spot because they are supposed to be the affordability bridge in the GTA, yet they are still absorbing the brunt of the repricing.

Family-grade supply is scarcer, which is helping detached hold value better than entry-level product.

Condos are supposed to be the affordability bridge. Right now, that bridge is still unstable.

So what is the right spring 2026 call?

Not collapse. Not recovery. Setup.

That is the right word. The market is coiled in the sense that supply is no longer flooding the system, sellers are still resisting weakness where they can, and there is clearly sidelined demand waiting for a better entry point. But that demand is still conditional. It needs cleaner price stability, better confidence, and fewer macro shocks.

Until that happens, this remains a buyer-leaning, negotiation-heavy market with selective strength, not a broad recovery market. Well-priced, scarce, high-quality homes can still sell well. Mispriced listings will still sit. Sellers anchored to old peak-market expectations will continue to lose time. Buyers who stay disciplined still have leverage in much of the market.

The corrected version of the original thesis is simple: the GTA market is coiled, but not cleared for rebound.

That is the real spring 2026 read: not bullish, not broken, just tight enough to matter and fragile enough to respect.

Source Base

-

TRREB Market Watch — February 2026

Primary GTA market structure, pricing, sales, listings, and product-type data.

-

Bank of Canada — January 28, 2026 Rate Decision

Policy-rate backdrop and macro policy framing.

-

Bank of Canada — January 2026 Monetary Policy Report

Tariff adjustment, geopolitical risk, and growth context.

-

Statistics Canada — Labour Force Survey, February 2026

Canada and Ontario unemployment conditions.

-

OREA / CREA Statistics — February 2026

Provincial sales, active listings, months of inventory, and benchmark pricing context.

CMS Notes

- This version is already stripped down to a pure embeddable HTML body block for CMS use.

- If your CMS strips the

<style>tag, move the CSS into your site’s custom CSS area and keep only the wrapper div and content markup. - The wrapper class

ow-market-blognamespaces the layout so it is less likely to conflict with your theme styles.